After 24 years of uninterrupted economic growth — and despite an increasing number of gloomy forecasts — Australia keeps defying gravity when it comes to booms and busts. Yet, sooner or later, as certain as death and taxes, Australia will face a recession.

After 24 years of uninterrupted economic growth — and despite an increasing number of gloomy forecasts — Australia keeps defying gravity when it comes to booms and busts. Yet, sooner or later, as certain as death and taxes, Australia will face a recession.

In this case, a crucial question is how well are we prepared as a nation to cope with a recessionary scenario?

To determine how much wriggle room Australia might have when the next crisis strikes, we can use a tool recently devised by The Economist — a tripartite indicator — to gauge the ability to fight recession.

Despite declining economic conditions and political paralysis, the indicator suggests Australia is still well placed compared to other developed nations — although much more could be done for the dog days ahead.

Such a ‘wriggle-room’ measure consolidates the arsenal power of fiscal and monetary flexibility to deal with a crisis, using three main statistics: fiscal space (i.e. the ability to raise public debt), budget balance and benchmark interest rate (cash rate).

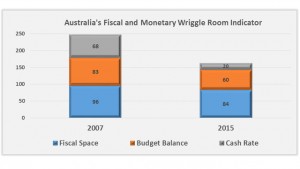

The chart above (Source: The Economist; RBA; Author’s calculation) shows Australia’s wriggle-room indicator at the brink of the GFC in 2007 in comparison to the latest numbers for 2015. For starters, in a similar movement to all the 22 nations followed in the analysis, Australia has visibly receded in its ability to fight a recession.

This is not a surprise. The rise of China and its voracious appetite for Australia’s minerals provided an unprecedented windfall in our terms of trade through the new millennium right up to the GFC, lifting national income and government revenues. On the other hand, global slowdown and particularly the fall in our export commodity prices — not to mention our own inability to reform — have incurred a toll on the economy in recent years.

Let’s start with fiscal space, an original IMF concept defined as ‘the difference between the current level of public debt and the [theoretical] debt limit implied by the country’s historical record of fiscal adjustment’. In short, it is the ability of a government to raise public debt over the medium and long-run without compromising its solvency.

A history of consistent — and accelerating — surges in both tax receipts and public deficits since the GFC have tarnished our ability to rely on more debt accumulation to counteract the effects of an eventual crisis. Hence, Australia’s fiscal space buffer has diminished from 96% of its theoretical debt limit before becoming insolvent (translating to 96 points in the 0–100 fiscal space metrics) in 2007 down to the current 84% (84 points).

The budget balance index goes from 100 points if a country runs a surplus of 5% or higher to 0 points for deficits of 15% or lower. Australia ran a 1.6% surplus in 2007 (83 points) as opposed the expected 3.1% deficit for 2015 (60 points). That is, unlike the onset of the GFC, our government will now have less room for short-run fiscal expansion.

The cash rate index explores the ability of the central bank to stimulate the economy by running monetary expansion through lowering the benchmark interest rate. Hence, the higher the starting cash rate level, the bigger the room for monetary stimulation: a score of 100 points is achieved for interest rates of 10% or higher down to 0 points for 0% (or lower as experimented recently) cash rates.

Australia finished 2007 with a cash rate target of 6.75% (68 points) — the highest level since 1996 — down to the current lowest historical level of 2% (20 points), which leaves practically very little room for the RBA to assist when the next recession comes.

Like every other indicator, there is always debate about the methodology. Some might comment that a cash rate of 10% is not consistent with the usual 2% inflation target; a crude budget balance does not differentiate infrastructure investments from other form of less productive spending; and the fiscal space concept runs on thin-ice concepts such as theoretical debt limits.

Notwithstanding all valid criticisms, the proposed wriggle-room indicator captures two important features of the Australian economy. First, we are not as prepared to fight another crisis as we were eight years ago. Second, Australia’s economy — despite all valid weaknesses — is still among the most resilient in the developed world. We might have lost the 2007 pole position ranking, but we are still among the top three, currently only behind to Norway and South Korea.

Having said that, no matter the relative position in the ranking, we should decisively move to implement a series of much-needed round of reforms (e.g. the Harper’s CPR recommendations) before the next crisis strikes. Pushing the luck of the lucky country is not a wise strategy; better to prepare for the worst, as hoping for the best might not help next time.

Home > Commentary > Opinion > When the recession comes

When the recession comes

In this case, a crucial question is how well are we prepared as a nation to cope with a recessionary scenario?

To determine how much wriggle room Australia might have when the next crisis strikes, we can use a tool recently devised by The Economist — a tripartite indicator — to gauge the ability to fight recession.

Despite declining economic conditions and political paralysis, the indicator suggests Australia is still well placed compared to other developed nations — although much more could be done for the dog days ahead.

Such a ‘wriggle-room’ measure consolidates the arsenal power of fiscal and monetary flexibility to deal with a crisis, using three main statistics: fiscal space (i.e. the ability to raise public debt), budget balance and benchmark interest rate (cash rate).

The chart above (Source: The Economist; RBA; Author’s calculation) shows Australia’s wriggle-room indicator at the brink of the GFC in 2007 in comparison to the latest numbers for 2015. For starters, in a similar movement to all the 22 nations followed in the analysis, Australia has visibly receded in its ability to fight a recession.

This is not a surprise. The rise of China and its voracious appetite for Australia’s minerals provided an unprecedented windfall in our terms of trade through the new millennium right up to the GFC, lifting national income and government revenues. On the other hand, global slowdown and particularly the fall in our export commodity prices — not to mention our own inability to reform — have incurred a toll on the economy in recent years.

Let’s start with fiscal space, an original IMF concept defined as ‘the difference between the current level of public debt and the [theoretical] debt limit implied by the country’s historical record of fiscal adjustment’. In short, it is the ability of a government to raise public debt over the medium and long-run without compromising its solvency.

A history of consistent — and accelerating — surges in both tax receipts and public deficits since the GFC have tarnished our ability to rely on more debt accumulation to counteract the effects of an eventual crisis. Hence, Australia’s fiscal space buffer has diminished from 96% of its theoretical debt limit before becoming insolvent (translating to 96 points in the 0–100 fiscal space metrics) in 2007 down to the current 84% (84 points).

The budget balance index goes from 100 points if a country runs a surplus of 5% or higher to 0 points for deficits of 15% or lower. Australia ran a 1.6% surplus in 2007 (83 points) as opposed the expected 3.1% deficit for 2015 (60 points). That is, unlike the onset of the GFC, our government will now have less room for short-run fiscal expansion.

The cash rate index explores the ability of the central bank to stimulate the economy by running monetary expansion through lowering the benchmark interest rate. Hence, the higher the starting cash rate level, the bigger the room for monetary stimulation: a score of 100 points is achieved for interest rates of 10% or higher down to 0 points for 0% (or lower as experimented recently) cash rates.

Australia finished 2007 with a cash rate target of 6.75% (68 points) — the highest level since 1996 — down to the current lowest historical level of 2% (20 points), which leaves practically very little room for the RBA to assist when the next recession comes.

Like every other indicator, there is always debate about the methodology. Some might comment that a cash rate of 10% is not consistent with the usual 2% inflation target; a crude budget balance does not differentiate infrastructure investments from other form of less productive spending; and the fiscal space concept runs on thin-ice concepts such as theoretical debt limits.

Notwithstanding all valid criticisms, the proposed wriggle-room indicator captures two important features of the Australian economy. First, we are not as prepared to fight another crisis as we were eight years ago. Second, Australia’s economy — despite all valid weaknesses — is still among the most resilient in the developed world. We might have lost the 2007 pole position ranking, but we are still among the top three, currently only behind to Norway and South Korea.

Having said that, no matter the relative position in the ranking, we should decisively move to implement a series of much-needed round of reforms (e.g. the Harper’s CPR recommendations) before the next crisis strikes. Pushing the luck of the lucky country is not a wise strategy; better to prepare for the worst, as hoping for the best might not help next time.

• Subscribe

Subscribe now and stay in the loop with our giving appeals, event alerts, newsletters and research updates.

We are always pleased to hear from you. If you have any questions or feedback, please contact us here: